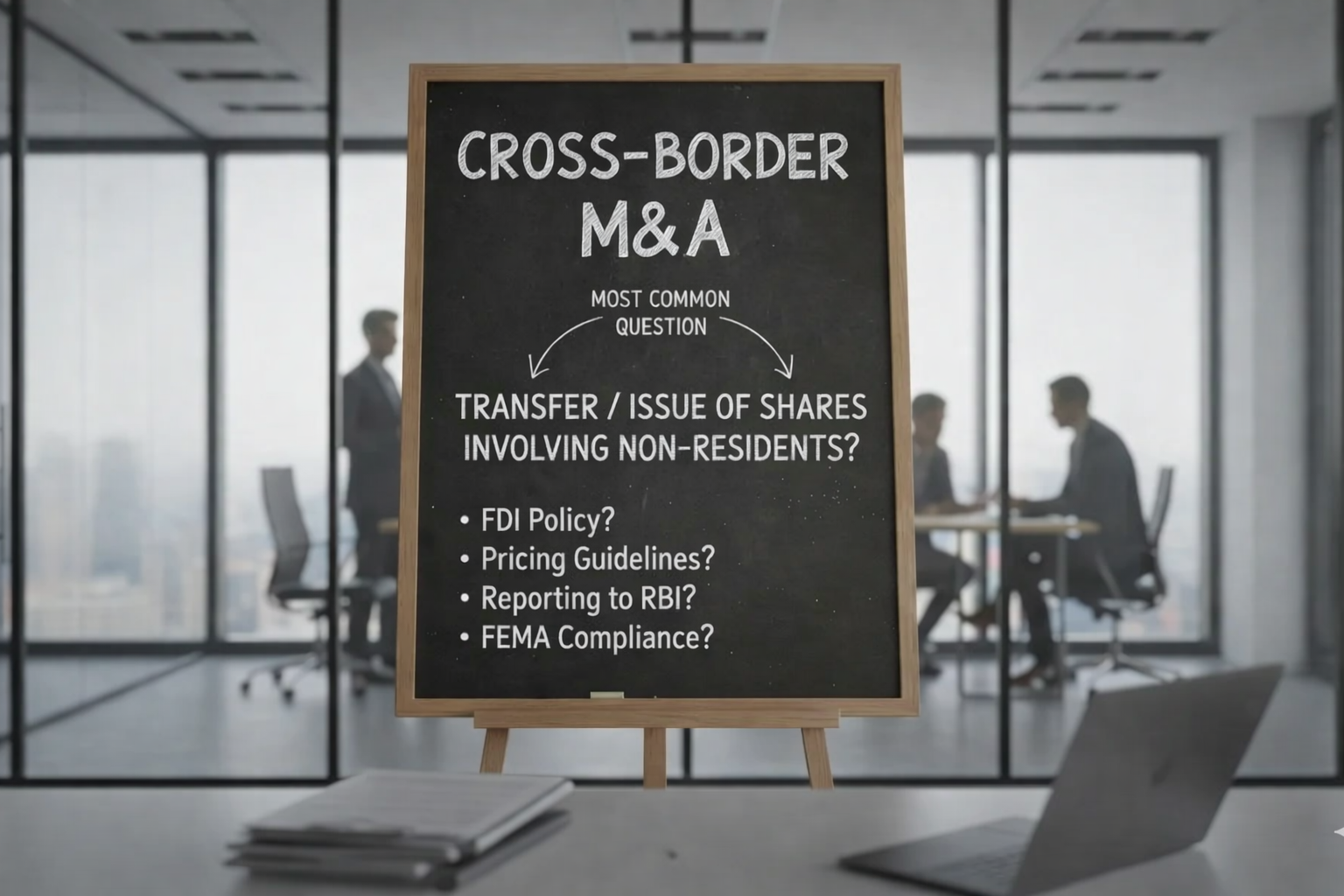

Most common question in cross-border M&A deals involving India

The question I get most often from global investors, in-house teams, or international law firms revolves around: the transfer / issue of shares involving non-residents.

𝗦𝗼𝗺𝗲 𝗰𝗼𝗺𝗺𝗼𝗻 𝘃𝗲𝗿𝘀𝗶𝗼𝗻𝘀 𝗜 𝗵𝗲𝗮𝗿:

• “𝘋𝘰 𝘸𝘦 𝘯𝘦𝘦𝘥 𝘙𝘉𝘐 𝘰𝘳 𝘍𝘌𝘔𝘈 𝘰𝘳 𝘰𝘵𝘩𝘦𝘳 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺 𝘢𝘱𝘱𝘳𝘰𝘷𝘢𝘭(𝘴) 𝘣𝘦𝘧𝘰𝘳𝘦 𝘵𝘳𝘢𝘯𝘴𝘧𝘦𝘳𝘳𝘪𝘯𝘨 / 𝘪𝘴𝘴𝘶𝘦 𝘴𝘩𝘢𝘳𝘦𝘴 𝘵𝘰 𝘢 𝘯𝘰𝘯-𝘳𝘦𝘴𝘪𝘥𝘦𝘯𝘵?

• “𝘞𝘩𝘢𝘵 𝘪𝘴 𝘵𝘩𝘦 𝘱𝘳𝘰𝘤𝘦𝘴𝘴, 𝘥𝘰𝘤𝘶𝘮𝘦𝘯𝘵𝘢𝘵𝘪𝘰𝘯 𝘢𝘯𝘥 𝘵𝘪𝘮𝘦𝘭𝘪𝘯𝘦𝘴 𝘧𝘰𝘳 𝘵𝘩𝘦 𝘴𝘢𝘮𝘦”

• “𝘈𝘵 𝘸𝘩𝘢𝘵 𝘴𝘵𝘢𝘨𝘦 𝘥𝘰𝘦𝘴 𝘰𝘸𝘯𝘦𝘳𝘴𝘩𝘪𝘱 𝘢𝘤𝘵𝘶𝘢𝘭𝘭𝘺 𝘱𝘢𝘴𝘴 – 𝘰𝘯 𝘴𝘪𝘨𝘯𝘪𝘯𝘨, 𝘱𝘢𝘺𝘮𝘦𝘯𝘵, 𝘰𝘳 𝘙𝘰𝘊 𝘧𝘪𝘭𝘪𝘯𝘨?”

• “𝘞𝘩𝘦𝘵𝘩𝘦𝘳 𝘢𝘤𝘲𝘶𝘪𝘴𝘪𝘵𝘪𝘰𝘯 / 𝘵𝘳𝘢𝘯𝘴𝘧𝘦𝘳 𝘸𝘪𝘭𝘭 𝘵𝘳𝘪𝘨𝘨𝘦𝘳 𝘰𝘱𝘦𝘯 𝘰𝘧𝘧𝘦𝘳?”

• “𝘈𝘳𝘦 𝘵𝘩𝘦𝘳𝘦 𝘢𝘯𝘺 𝘱𝘳𝘪𝘤𝘪𝘯𝘨 𝘳𝘦𝘴𝘵𝘳𝘪𝘤𝘵𝘪𝘰𝘯𝘴 𝘧𝘰𝘳 𝘵𝘩𝘦 𝘥𝘦𝘢𝘭?”

The answer lies in the Companies Act, 2013, Indian foreign exchange control laws, SEBI norms, anti-trust laws and the Articles of Association, backed by the applicable secretarial process.

• FEMA/RBI approval – for transfer / issue of shares involving non-residents, where pricing or sectoral caps are breached, or where the transfer falls under the approval route (e.g., defence, telecom, insurance, etc.).

• DPIIT or FDI nods – when investments come from countries sharing land borders with India.

• Competition Commission of India – for combinations exceeding the prescribed asset or turnover thresholds.

• Sectoral regulators (IRDAI, SEBI, RBI) – in case of regulated entities like NBFCs, insurers, or listed companies.

A share transfer / issue may look procedural, but it is often the legal pivot point of an M&A deal. Gaps in approvals or filings can surface as due diligence red flags, delay deal closing, or even compromise ownership validity.

Having advised on multiple inbound and outbound deals, I have found that early regulatory mapping before signing can save weeks at closing.